Counterfeiting Benefits Counterfeiters (and Harms Everyone Else)

The title of this post may seem obvious, but it’s a point that often gets lost in the discussions over monetary policy. To be clear, I’m not saying central banks are violating the laws of their countries. Rather, in this post I’m going to make some obvious points when it comes to the impact of private sector counterfeiters, which should then help clarify the confusion surrounding central bank inflation.

Motivating the Discussion

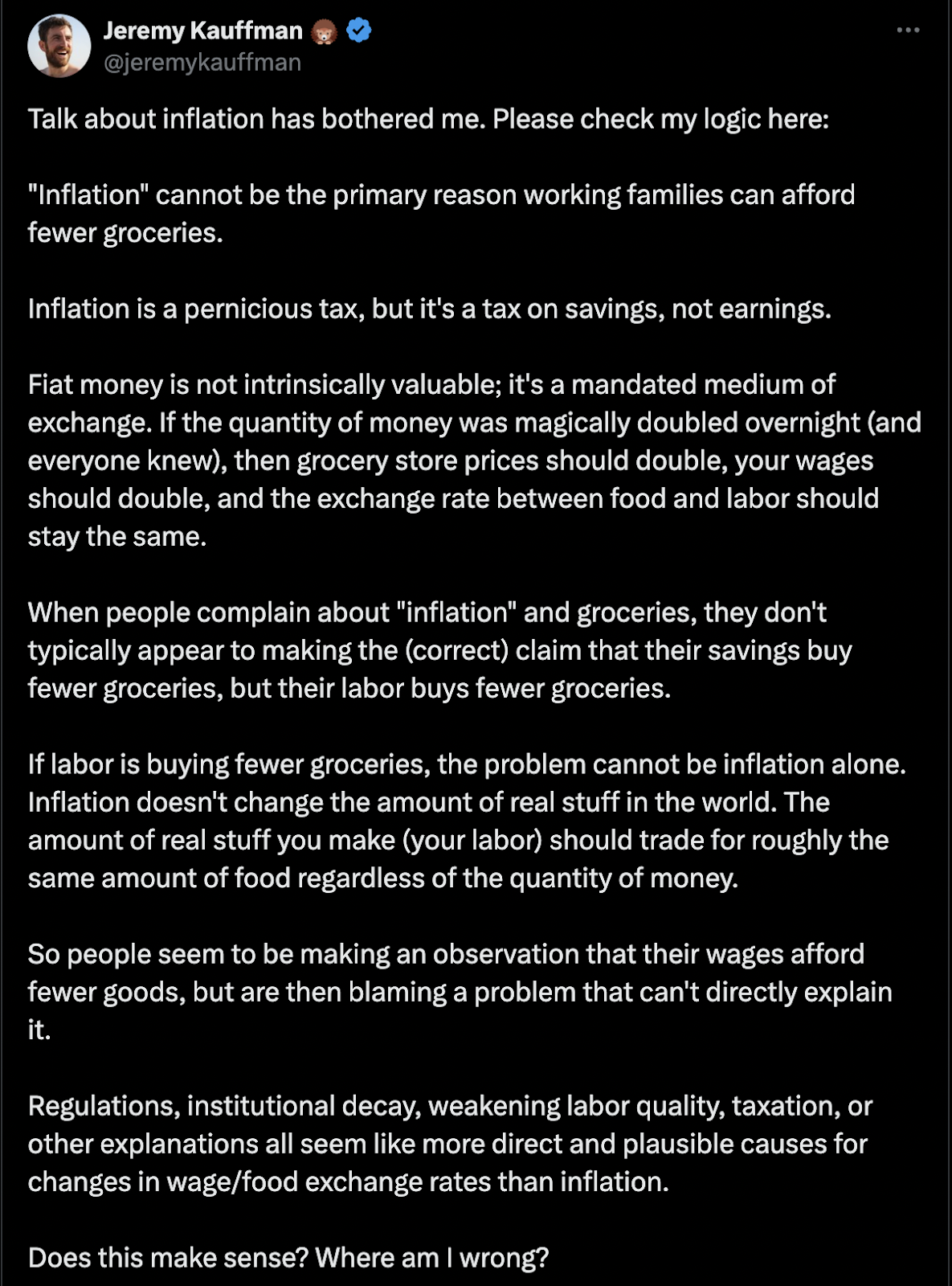

The specific motivation for my post comes from a puzzle that a libertarian activist tweeted out over the weekend:

To be clear, I’m not picking on Kauffman in my response. (I answered him directly on Twitter but will be more comprehensive here.) But he crystallized the issue with his question, and lots of people have similar takes, on both the left and right ends of the American political spectrum.

For example, when making their case against the Fed, fans of Ron Paul often post graphs of the collapse in the US dollar’s purchasing power, such as this:

In response, both progressive and conservative/libertarian critics will often guffaw, and argue that nominal wages and salaries are much higher now, then they were back in 1913, and precisely because of the “currency debasement.” The implication is that it’s all just a wash, and that at worst Fed monetary inflation might redistribute wealth out of people’s bond portfolios, but not by making their paychecks weaker at the grocery store.

In the rest of this post, I’m going to explain why that conclusion is wrong. If a counterfeiter lived down the street from you, his activities wouldn’t simply reduce the (real) value of your bond coupon payments. It would also mean the ongoing payment for your labor services wouldn’t keep up with retail prices.

Carl the Counterfeiter

Suppose Carl lives down the street from you, and that he has perfected a printer in his basement that cranks out $100 bills that are indistinguishable from the real thing. Carl quits his job and every month prints out a fresh $1 million that he uses to buy goods and services that the rest of us continue to produce, month in and month out.

First (and easy) question: Does this practice enrich Carl, from the standpoint of his material standard of living? Yes, of course it does. He now can buy $12 million worth of goods and services (if he just focuses on consumption) each year, without having to work for it. This might be corrosive to his soul, but it definitely benefits him in a straightforward way.

Second (and harder) question: Does this practice affect everyone besides Carl? Well, unless you think that Carl’s counterfeiting operation somehow boosts total economic output, it obvious must be the case that Carl makes everyone else on average suffer a hit to the standard of living. If Carl is consuming more, and the total pie hasn’t increased, then it must be the case that everyone else is consuming less.

A Tax Analogy

In response to my initial response to his tweet (analogous to the one I gave above), Kauffman followed up by pointing out that the economic impact of the counterfeiting should be the same as if the government levied a direct tax of $12 million. (I’m adjusting the numbers to fit my example here in this post.) And levying a tax shouldn’t change the market exchange rate between an hour of labor and jars of peanut butter, so how does my story fit the bill?

I pointed out that yes, an explicit tax wouldn’t (by itself) directly affect the number of jars of peanut butter you can buy with one hour of your labor, if we are looking at your gross paycheck. But of course, once we take into account that you have explicit taxes taken out of it, then of course your net pay doesn’t get you as much peanut butter as you would be able to afford in the absence of the tax.

When the government explicitly taxes (say) $12 million from the community and gives it to Carl, that obviously makes Carl $12 million richer and everybody else $12 million poorer. (We are ignoring incentive effects because of the tax, etc., and just looking at the immediate, direct impact.) But there’s no reason for prices to rise, because the quantity of money is the same; the government just takes some of it from the community and hands it over to Carl.

But if instead the government prints up a new $12 million and hands it to Carl, then everybody else still has their full gross paycheck. It still must be the case, however, that they can afford to buy fewer jars of peanut butter to make it physically possible for Carl to buy more. (After all, the government printing up $12 million doesn’t make the economy able to generate more peanut butter per month.)

In the case of an “inflation tax,” the mechanism by which this fleecing occurs is that people find their paychecks don’t go as far at the store. So it must be the case that the average person finds his or her income failing to keep pace with the general increase in retail prices. Now depending on your model of how the economy works, the specific transmission mechanism would look different. I am merely making the modest, yet critical, point that if counterfeiting allows some members of the community to become richer, then it must mean everybody else sees prices rise faster on the items they typically buy, than their own incomes rise.

Complications

Now that I’ve made my basic point, let’s deal with some complications. First, depending on your macroeconomic views and the context, we can imagine monetary inflation raising total economic output in the community. For example, if gold is the money, I don’t think gold mining is a pure transfer of wealth from everyone else to the miners, even if we focus purely on the gold being used for monetary purposes. Or for another example, I don’t think Satoshi made the-rest-of-humanity poorer by releasing his (her?) white paper and presumably sitting on a bunch of bitcoins. Having said all of that, it is clear that this type of complication isn’t what Kauffman or Ron Paul’s critics have in mind, when they say currency debasement can’t depress real wages.

That leads to the next complication: How can I, as a free market economist, possibly argue that workers in a competitive system don’t earn the marginal product of their labor, just because the Fed is printing up money? This is a difficult topic, and I actually wrote a book chapter on it (for a volume that alas has not yet been published for various reasons). If it makes one feel more consistent, we can agree with Kauffman’s original take by pointing out that when you get paid wages from your employer, that addition to your checking account is technically your “savings” until you spend it. So however you want to model the situation, so long as there exists a new equilibrium in which the value of the money doesn’t immediately drop to zero, then it still must be the case that real wages (for those not directly connected to the counterfeiting) permanently lag behind.

Incidentally, this is why I don’t react negatively—as other libertarians often do—when progressive think tanks argue that real wages have stagnated for decades. These think tanks want to blame Ronald Reagan’s tax cuts and deregulation, but I point out that their own charts actually show it was Nixon leaving the gold standard that best explains the phenomenon.

Finally, mainstream economists often argue that “seigniorage” (the technical term) is a real thing, but in the United States doesn’t amount to much in the grand scheme. For example, in a 2022 column Paul Krugman estimated that the US government only monetized about $150 billion of its deficit in 2021. Now he came up with that number by focusing merely on the actual green pieces of paper that were newly issued. Yet in reality, the Fed added about $900 billion on net of Treasuries (I’m ignoring the mortgage-backed securities) to its balance sheet in 2021, which certainly helped to finance the massive new debt that the Treasury issued during the Covid era. You can read Krugman’s column to see his justification for his decision, but it seems obtuse to ignore the huge influx of bank reserves (not just paper currency) that the Fed created in this period.

In any event, if Krugman and other mainstream economists want to argue that possessing the printing press is no big deal, then I gladly volunteer to take it over. After all, wages and contracts all adjust once the public gets a sense of the inflation rate, right?

NOTE: This article was released 24 hours earlier on the IBC Infinite Banking Users Group on Facebook.

Dr. Robert P. Murphy is the Chief Economist at infineo, bridging together Whole Life insurance policies and digital blockchain-based issuance.

Twitter: @infineogroup, @BobMurphyEcon

Linkedin: infineo group, Robert Murphy

Youtube: infineo group

To learn more about infineo, please visit the infineo website

Comments