Recession Warning from the Index of Leading Economic Indicators

In early August, I published a post making the case against a “soft landing” for the US economy. At that time, I focused on interest rates (especially the inverted yield curve). Also, I showed how the ostensible signs of optimism given by the soft landing crowd were present right before the 2008 crisis.

In the present post, I’ll adopt a similar strategy: First, I’ll document that the Conference Board’s Index of Leading Economic Indicators — which includes the yield curve but several other indicators as well — has been flashing red for quite some time. Second, I’ll address the argument (made in particular by the Modern Monetary Theory, or MMT, camp) that the large federal budget deficits are the reason “this time is different.” As we’ll see, I don’t think transferring savings to Washington DC is the way to revive a sick economy.

The Index of Leading Economic Indicators

The Conference Board publishes its well-known Index of Leading Economic Indicators. Here is how the Conference Board itself describes its index:

The LEI is comprised of 10 indicators that cover a wide range of economic activity, including job growth, housing construction, and stock prices. The index is designed to provide a broad-based look at the health of the economy and can be used to predict turning points in the business cycle. The LEI acts as a predictor of turning points because as a composite index it summarizes the consensus of forward-looking indicators from different areas of economic activity.

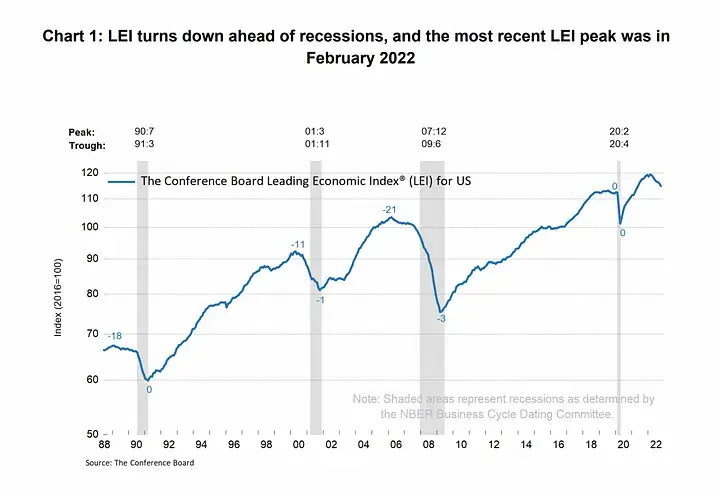

Then, to see the historical relation between downturns in the LEI and actual recessions, the same post provides this chart:

Incidentally, the above chart only shows data through October 2022. As of the most recent (October 19, 2023) update, with data through September 2023, the LEI has continued to fall every month, with a current reading of 104.6 (using the same baseline as in the above chart).

As the chart above shows — and especially if you mentally extend the downward blue line to 104.6 — downturns in the LEI of this magnitude have always led to recession soon after. So if there isn’t a recession in 2024, not only will it be the starkest violation of the yield curve’s track record, but it will also be a similarly unprecedented outcome vis-a-vis the index of Leading Economic Indicators.

Deficit Spending to Save the Day?

To be sure, I’m not the only one who knows about inverted yield curves and the LEI index. Many economists and analysts were quite confident that we already would have seen a recession by now — in fact, Bloomberg in 2022 said it was a certainty! But with the continued rosy unemployment figures and moderating CPI inflation readings over the summer, the general pessimism turned to mild and growing optimism. What explains the Fed’s ability to apparently thread the needle?

One answer, especially popular with the MMT camp, is to say that the Fed’s rate hikes — coupled with far more outstanding Treasury debt than was the case back in the late 1970s when Volcker slammed on the monetary brakes — have ironically led to a huge influx of income from the Treasury. In other words, some analysts are arguing that with our current sovereign debt load, Fed rate hikes are expansionary. (In this video, I showcase and critique Warren Mosler’s presentation of this claim.)

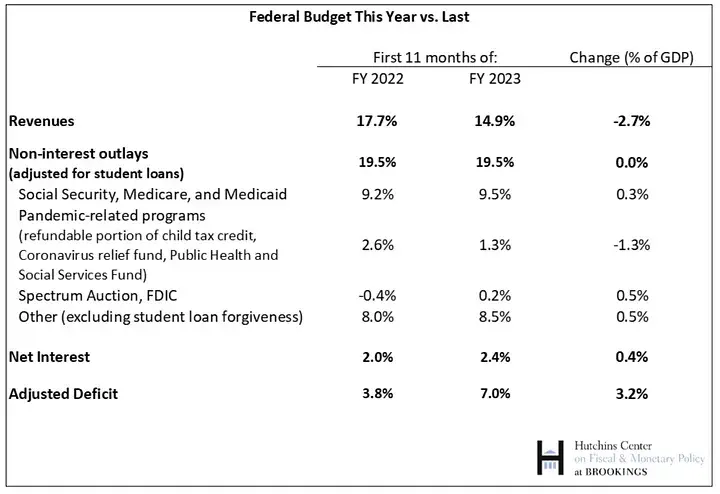

Whatever one thinks of the MMT claim on theoretical grounds, their explanation is misleading because the massive rise in the deficit (relative to last year) wasn’t primarily due to interest rate hikes. In a September 2023 post for the Brookings Institution, Louise Sheiner breaks it down:

As the table indicates, although net interest payments were 0.4% of GDP higher in (the first 11 months of) Fiscal Year 2023 compared to the same period in FY 2022, increases in other programs were higher, and the year/year drop in revenue at 2.7% of GDP was a much bigger factor. (Sheiner gives some of the causes for the drop in revenue, which include lower capital gains due to the stalling stock market, as well as a tax filing extension for residents of California due to extreme weather.)

Conclusion

In the present post, I won’t give the basis for my entire economic worldview from scratch. Suffice it to say, if you are the type of person who generally believes that the private sector does a better job allocating resources than the government, then learning more of the specifics of the US’s fiscal position shouldn’t reassure you.

The inverted yield curve and a plunging index of LEI are historically good guides to warn of an impending recession. The fact that the Treasury just borrowed $1.7 trillion in Fiscal Year 2023, while the Fed’s balance sheet has been steadily shrinking since March 2023, does NOT lead me to conclude, “This time will be different.” I still believe we are in store for a recession that will (perhaps after a lag) be clocked as having started in the first half of 2024.

NOTE: This article was released 24 hours earlier on the IBC Infinite Banking Users Group on Facebook.

Dr. Robert P. Murphy is the Chief Economist at infineo, bridging together Whole Life insurance policies and digital blockchain-based issuance.

Comments