The Problems With Kamala Harris’ Anti-“Price Gouging” Proposal

Vice President Kamala Harris has proposed a federal ban on price gouging in certain sectors of the economy, such as food and groceries. This is an utterly misguided plan, which fails to address the real reasons for rampant price inflation, and if sufficiently enforced will lead to food shortages.

Food Price Inflation

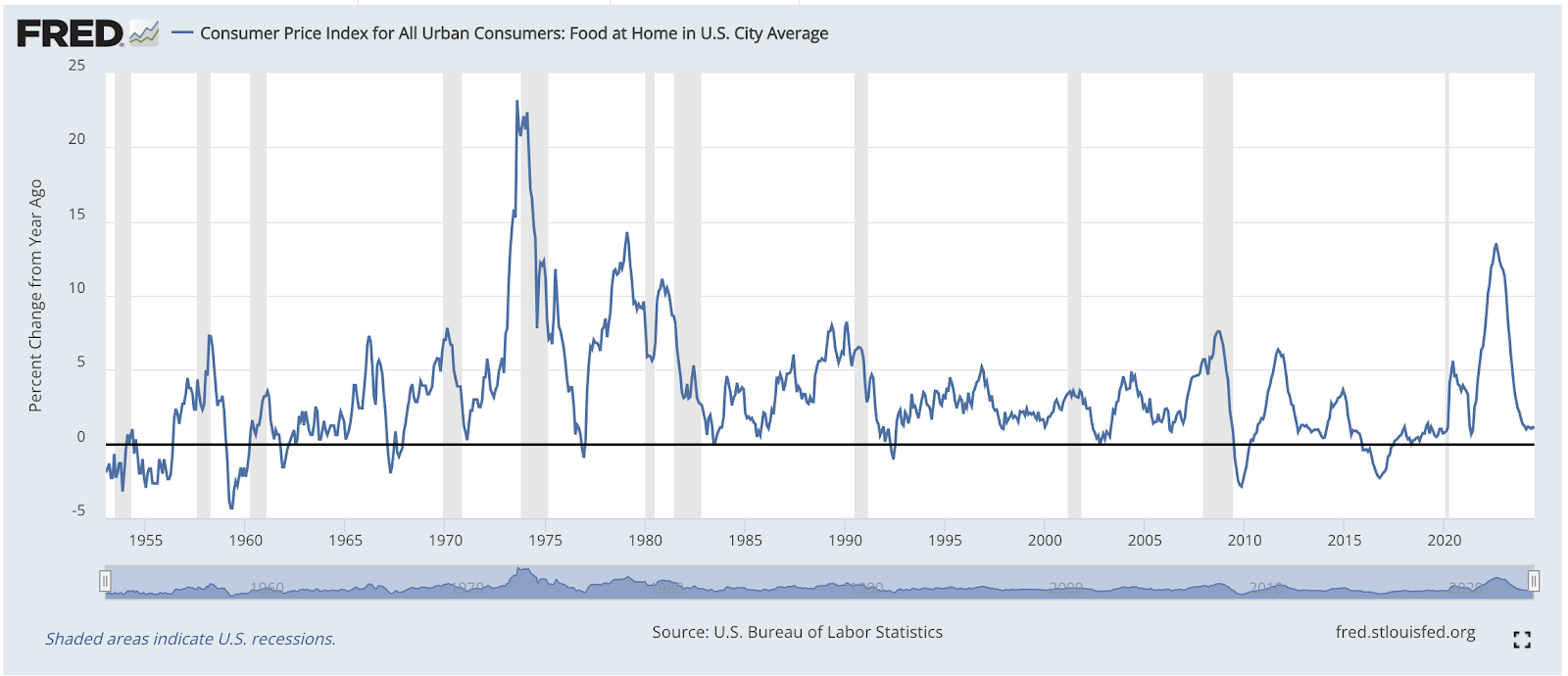

The first order of business is to document that you’re not imaging things: food prices have been skyrocketing. Specifically, the year-over-year increase in the “Food at Home” component of the Consumer Price Index (CPI) peaked at 13.5 percent back in August 2022, which was the highest 12-month jump since February 1979:

Although the rate of increase in food prices has returned to normal, the level of food prices (according to this particular metric) is still 27 percent higher than five years ago (in 2019, before Covid). At this point I should stress that we are here relying on government statistics; many people—myself included—think that these “official” numbers are suppressing the actual hike in food prices. Among other issues, if the official metrics fail to adequately take account of “shrinkflation” and other ways of cutting costs—such as very thin cardboard boxes for cereal compared to pre-pandemic levels—then the chart above is not adequately conveying the full story.

Price Inflation Is Due to Monetary Inflation, Not “Greed”

Before we figure out what—if anything—government officials should do about the price of food, it would make sense to first understand what caused the recent bout of unusually rapid hikes. The standard progressive bogeymen of “corporate greed” and/or “market power” don’t really fit the bill; at best they are akin to blaming a plane crash on gravity. If we want to know why food prices rose so much in 2022 specifically, then generic explanations don’t really help. After all, it’s not as if corporations became greedy that year, and then returned to their normal posture of selflessness a year later. It’s the same with market power or industry concentration; these aren’t factors that ramped up in 2022 but subsided after a year.

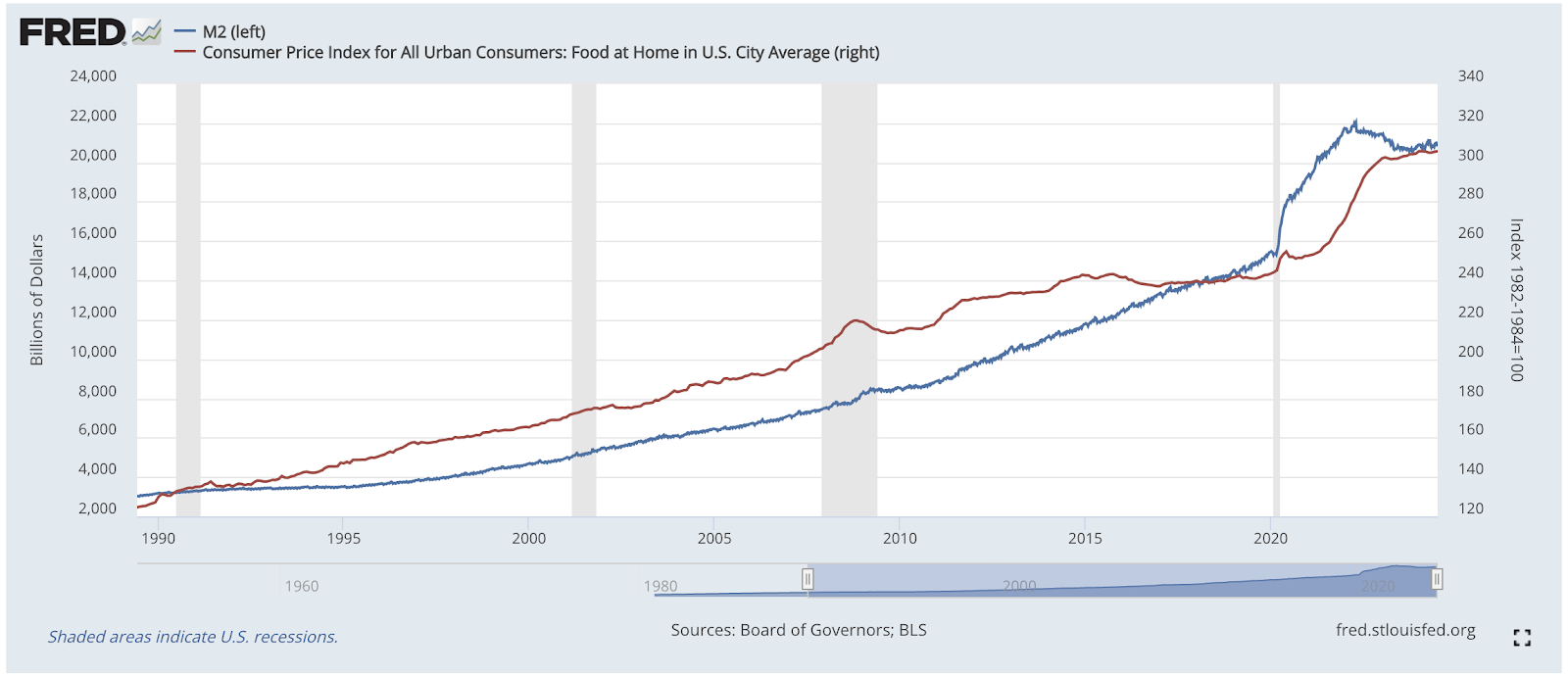

In contrast, the economists who blamed (at least in part) loose monetary policy can explain the vicissitudes of food price inflation. The following chart plots the M2 monetary aggregate (blue line) against the level of “food at home” prices (red line):

As you can see, the connection isn’t perfect, but the big jump in food prices—as well as their tapering off—went hand in hand with a similar move in the money stock.

It’s not a wacky theory to suggest that when the Fed dumped boatloads of money into the economy right when the lockdowns took hold, that this started pushing up prices. This would especially make sense for “food at home” prices, because it was literally illegal to go out to restaurants for a stretch, and even afterwards many people preferred to dine at home, compared to pre-pandemic patterns.

Standard Price Ceilings Cause Shortages

As a professional economist, it is part of my contractual obligation to post a chart whenever we talk about price controls. The following diagram (and the accompanying two paragraphs of text) come from my own textbook Lessons for the Young Economist (available in free pdf from the Mises Institute):

The general pattern is the same whether we are talking about apartment units (the example I used in my textbook) or grocery items. If the market-clearing price is a certain level, and then the government makes it illegal to charge that amount, the policy will likely cause shortages.

This isn’t an abstract economic theory. This has happened throughout history and around the world, whenever governments dump extra money into the system and then punish merchants for raising prices in the face of the new demand. The gasoline lines in the US in the 1970s weren’t due to OPEC, but to the Nixon Administration’s price controls. And the massive food shortages in Venezuela are likewise due to the one-two punch of hyperinflation coupled with sanctions on price hikes.

When the central bank (which is the Federal Reserve in the US) opens up the monetary spigots, commodity prices typically respond immediately. Therefore the input costs of making the food items that end up in grocery stores, are much higher now than in 2019. If grocery stores hadn’t been allowed to raise prices accordingly, it’s not that they would have continued to sell milk, eggs, and bottled water at a loss; they would’ve simply stopped stocking the shelves. Again, this isn’t some pointy-headed theory; this happens all the time whenever we mix money printing with price controls.

What About “Record Profits”?

Many pundits will concede the basic story I’ve told above, but they will respond with the following argument: “Sure, if grocery stores and other companies with market power were simply passing along cost hikes, then government penalties on retail price increases would cause the shortages you’re warning about, Murphy. However,” they might continue, “in the real world that’s not what’s happening here. A lot of greedy corporations were using the Covid supply bottlenecks as an excuse to jack up prices. That’s why plenty of firms are enjoying record profits right now—because they raised their own customers prices far more than their own costs went up.”

However, let’s get some perspective here. It is true that official measures of grocery store profit margins hit record highs during in recent years. But that’s a very misleading statement for two reasons. First, grocery profit margins in 2023 had fallen back to 1.6 percent, the lowest level since the 2019 figure of 1 percent. Second, we can’t just talk about the relative levels, we need to say the absolute amount: Even at their peak in 2020, the grocery industry profit margin was a whopping…wait for it…3 percent.

During the Covid lockdowns and aftermath, there was an incredible upheaval in the global economy. Many businesses failed while others prospered—either for “fundamental” reasons or simply because they were politically connected. In general, the profit-and-loss system gives rewards and penalties to those entrepreneurs who saw the future better (or worse) than their peers.

So yes, during a massive disruption both in supply chains and the pattern of consumer demand (people ordering exercise bikes from Amazon and meals from Uber eats, etc.), many businesses will go down but those that happened to be ideally positioned would see above-average profits. That is what you would expect to see even if the Fed hadn’t dumped boatloads of new money into the system, and hence even if CPI inflation had been within historical norms.

It's not a popular thing to say, but unusually high profits are exactly what we want to accrue to those individuals and businesses that respond quickly to a crisis. When there’s a hurricane or other natural disaster, we want bottled water and gasoline prices to spike. This serves a two-fold purpose: First, it incentivizes consumers to only buy what they really need—for example, people with half a tank of gas might drive 100 miles inland to see if they can find cheaper prices before filling up, which allows the limited gasoline in a coastal area to be more uniformly rationed among the vehicles trying to flee. Second, it incentivizes suppliers to rush emergency items to the region. If bottled water is selling at a 1,000% markup in a flood zone, guys with pickup trucks in neighboring states might start making runs. Yes, that might strike some as unconscionable gouging, but if the Attorney General cracks down on the practice, it doesn’t mean those same guys will take two days to bring trucks of water in for normal retail prices—no, they’ll just send their thoughts and prayers while they scroll to the next item in their news feed.

To sum up: Kamala Harris’ proposed ban on “price gouging” doesn’t address the real culprit, namely the Federal Reserve with its loose monetary policy. Given how much money was dumped into the system, cracking down on price hikes will only cause shortages.

NOTE: This article was released 24 hours earlier on the IBC Infinite Banking Users Group on Facebook.

Dr. Robert P. Murphy is the Chief Economist at infineo, bridging together Whole Life insurance policies and digital blockchain-based issuance.

Twitter: @infineogroup, @BobMurphyEcon

Linkedin: infineo group, Robert Murphy

Youtube: infineo group

To learn more about infineo, please visit the infineo website

Comments