The USD Weakens When Foreigners Dump It

As with last week’s post—which was named “Counterfeiters Benefit From Counterfeiting”—the title of today’s installment may seem obvious. After all, if foreigners want to reduce their holdings of the USD (and more generally, USD-denominated assets), wouldn’t that clearly result in a weakening of the dollar against their respective currencies?

To me it is crystal clear. However, over the course of the year I’ve been in continual discussions with Brent Johnson (of “Dollar Milkshake” fame) and George Gammon (of “Rebel Capitalist” fame), and I’ve seen that there is still a great deal of controversy on this topic, stemming from the dollar’s special role in global finance. As Brent spelled out to me during our debate on ZeroHedge back in February, the extensive “Eurodollar” system complicates things, so that a normal supply/demand analysis might spit out the wrong answer, at least in the short- and medium-run.

Specifically, Brent and his supporters have been arguing that because so many foreigners currently own USD claims issued by other foreigners, any move by the-world-outside-the-United-States to reduce its net holdings of USD assets will involve a deleveraging crunch. Since the foreigners who owe US dollars can’t just print up the money (i.e. they aren’t the Fed), this process will involve a deleveraging squeeze that will lead to a scramble in the currency markets for genuine USD. Paradoxically, Brent et al. conclude, even if the globe wanted to reduce its dependence on King Dollar, the very act of dethroning it would lead to a rising dollar in the forex markets.

To be clear: Although I very much respect Brent, George, and others in this discussion, I think their analysis on this point is wrong. Back in March I invited Brent onto a podcast I host for the Mises Institute to hammer out our differences, and then here at infineo I posted an article trying to explain my problem with his perspective. As the continued discussions on Twitter indicated, my attempts were unsuccessful. But after the latest round of back-and-forth, I understand better where the confusion is occurring. So allow me to post some of Brent’s latest commentary below, giving his perspective in his own words, and then I’ll try again to show why (I believe) he is mixing up two related, but distinct, processes.

Brent Johnson on Dollar Deleveraging

The recent Twitter flare-up occurred on August 29 when Brent—whose account is named after his company, Santiago Capital—made the following connection between de-dollarization and deleveraging:

In response to the above, I said that although I respected Brent, I thought his particular claim here was “nuts.” Brent and others pushed back against me, leading me to play a Reverse card, to which Brent also replied, like so:

To drive home the essential point, someone else chimed in, elaborating on the deleveraging element. As you can see, Brent enthusiastically agreed:

I believe the above screenshots are sufficient to demonstrate what Brent (and his fans) are arguing here. To repeat, I believe there is an important element of confusion behind their stance: Specifically, Brent et al. are mixing up two different things. They keep focusing on (A) a reduced demand to hold a particular type of claim on USD with (B) a reduced willingness to hold any dollar denominated asset.

Part of the difficulty in the analysis of the so-called Eurodollar system is that foreign institutions issue claims “out of thin air,” to an underlying item that is itself issued “out of thin air” by the Federal Reserve. In order to solidify my perspective, I think it will be most useful in the rest of this post to focus on something tangible. For that reason, we now proceed to analyze the global demand to hold bars of gold as a “reserve” asset.

The Global Demand for Gold: Assume Full Reserves

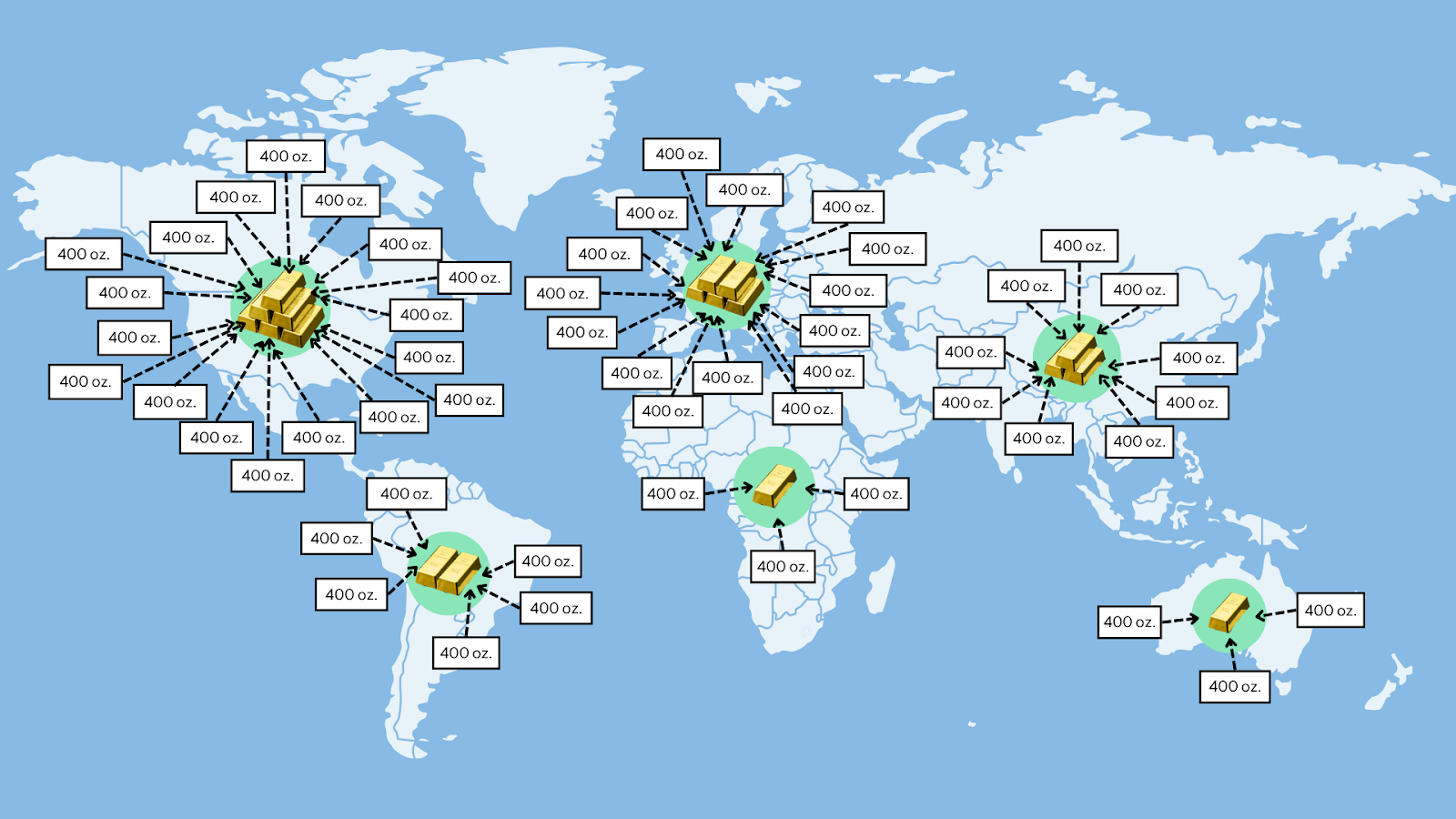

Let’s first analyze the situation with the assumption that any institution holding gold has the actual yellow metal, or that it holds legal claims on gold that are backed up 100% (with gold in the vault) by the party issuing the claim. Consider the following map

Map 1: Global Demand to Hold Gold, Full Reserves, World Price of $2,500/oz.

In the above Map 1, the story I have in mind is that there is a widespread demand from institutions around the world to hold gold as a monetary reserve asset (a hedge against local inflation, if you want to be specific). The biggest stockpiles are in the United States and Europe, with Asia in the middle and then thinning out as we look at South America, Africa, and Australia. We assume at this stage that all of the people holding gold have the actual hunks of yellow metal in their physical possession (or that of trusted custodians who have bailment contracts).

Let’s suppose that in this initial equilibrium, the world price of gold is $2,500/oz. Given everybody’s costs of inventory management, and more crucially, their expectations of future market conditions, at this world price, the total quantity demanded to hold gold is exactly equal to the sum total of the physical stockpiles of gold bars.

Now suppose this original equilibrium is disturbed when—for whatever reason—the institutions in the outlier regions decide they no longer want to hold gold as a reserve asset. Consequently they dump their gold stockpiles and use the proceeds to buy other assets. After the dust settles, and the gold finds its way into the vaults of people who do still want to hold it, the global map looks like this:

Map 2: Regional Demand to Hold Gold, Full Reserves, World Price of $2,000/oz.

In Map 2, we see that the physical amount of gold on planet Earth hasn’t changed. The bars that originally were in vaults in South America, Africa, and Australia have simply migrated into the US, Europe, and Asia, augmenting their original stockpiles.

However, such a reshuffling of gold stocks—when we know that in this fictional example, the cause was the evaporation of gold demand in three of the continents—will lead to a fall in the new world price of gold. At the original price of $2,500/oz., the institutions in the US, Europe, and Asia were holding their desired quantities, and so to induce them to absorb more gold into their inventories, the current spot price must clearly fall. We obviously picked $2,000/oz. as the new price because it was a nice round number, but there is no doubt that whatever the new price is, it will be lower than the original price. Again, given that the original owners in South America, Africa, and Australia are dumping their stockpiles, it must be the case that the global price of gold falls in order to make the other regions acquire more, seeing a buying opportunity when gold appears “cheap.”

The Global Demand for Gold: Assume Only Fractional (One-Third) Reserves

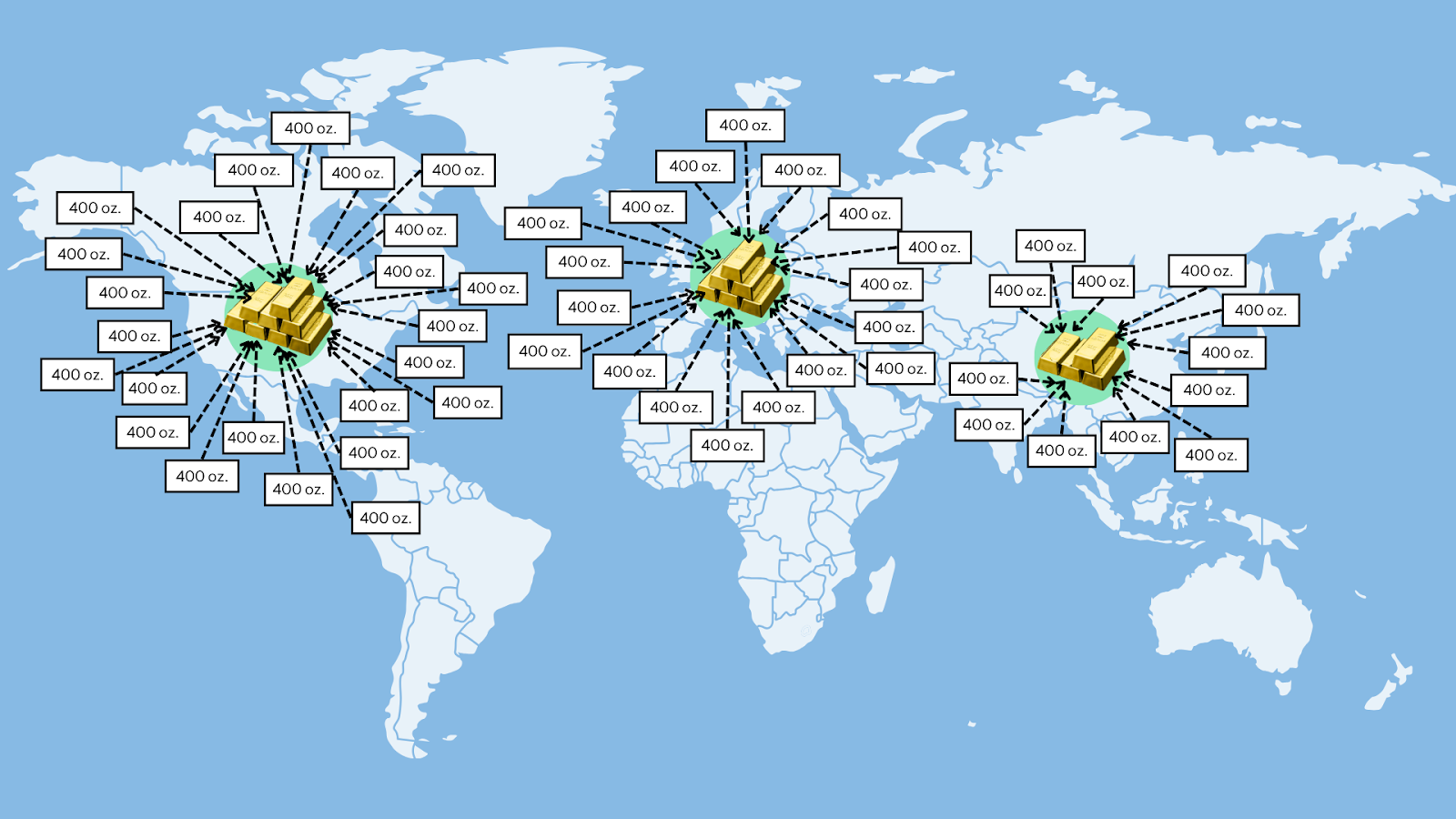

Let’s tell a similar story, but this time we assume that in each region, institutional buyers of gold can hold either the physical metal, or they can hold claims on gold. Furthermore, these claims are not backed 100 percent, but instead only have (say) a one-third backing. The situation looks like this:

Map 3: Global Demand to Hold Gold, One-Third Reserves, World Price of $2,500/oz.

In Map 3, we have returned to our original scenario, but we’ve introduced a layer of complexity. Rather than assuming every institutional holder of gold has a direct one-to-one connection with the physical metal, we now assume that the institutions hold legal claims on the underlying gold. Furthermore, we assume that these claims in the aggregate are only “backed up” by a third; a “run on the bank” could cause redemption problems.

However, at the snapshot of Map 3, all is calm. On the margin, anyone wanting to redeem his notes can transform them into a chunk of yellow metal, and so the notes trade at the same market price as the underlying physical commodity. This makes it easier for institutional and even retail customers to obtain exposure to gold as an asset class, because it’s much easier to trade legal claims to gold, rather than moving the physical bars from vault to vault. As before, we assume in this initial situation that a world price of $2,500/oz. equates the quantity supplied and demanded, bearing in mind that “quantity” here refers to the notional amount represented by the outstanding notes.

Now what happens if, as before, we assume that the demand to hold gold as a reserve asset fades away in some of the regions? The owners of physical gold and notes in South America, Africa, and Australia sell them for other assets. When the dust settles, the world looks like this:

Map 4: Regional Demand to Hold Gold, 1/3 Reserves, World Price of $2,000/oz.

As indicated in our final Map 4, the introduction of fractional-reserve gold claims doesn’t alter the basic story. As owners in three continents begin selling off their gold holdings, buyers in the remaining regions snatch them up. However, the global price of gold has to fall to facilitate this shuffling of ownership.

The fractional backing of the circulating gold notes is a complication, to be sure, but that complication doesn’t alter the basic fact that when fewer people on Earth wish to hold gold as a reserve asset, the world price of gold must fall in order to induce others to add to their pre-existing inventory.

Of critical relevance, given the context of this article: Especially if the process is gradual, there is no reason to suppose that the fractional backing will change: We still have one-third reserves backing up the outstanding gold notes, it’s just that the owners of the metal bars and the legal claims have changed. In other words, the mere fact that some of the original gold holders have a change of heart, does not imply “deleveraging” in the gold market.

Remember: In this scenario, it’s not the case that the original holder of a 400oz. note in (say) South America, wants to redeem that note for a bar of gold and hold the physical metal instead. If that were the case, then yes, there would be a crunch in the South American gold market, as debtors rushed to obtain the metal to redeem their obligations. But in our scenario, the South American note holders don’t want to hold physical gold either. It’s not that they’re running away from claims on gold, they don’t want to hold gold itself. And so rather than redeeming their notes for the real thing, instead they will sell the notes outright to some other buyer. In our example, we assume those buyers are located in other countries, and that’s why the gold—and notes—migrate north.

Confusion About Dollar De-Leveraging

The tweets I shared above—and others like them—underscore a confusion in this discussion. In an economic crisis, it is quite natural for market players to rush to liquidity. In the midst of a panic, it’s much better to have five Ben Franklins in your home safe, rather than an electronic checking account balance of $500 with your local bank. This is particularly true if you live outside of the United States, where the authorities have no legal ability to generate an extra $500 by fiat.

Consequently, economic shocks can often lead the holders of certain types of USD-denominated assets to prefer to transform them into more liquid forms of USD-denominated assets, such as Treasuries, checking balances with American banks, or even physical currency. I believe this is the type of scenario folks like Brent Johnson have in mind, when they are thinking that foreigners who owe USD to others, could effectively have their loans called, and then scramble to come up with the real thing.

I have no problem with any of this reasoning. And indeed, it wouldn’t surprise me if an economic shock in, say, the year 2025 leads global investors to rush to more liquid forms of USD assets, which puts the squeeze on those who are short the less liquid forms, and consequently drives up the value of the USD in the forex markets.

But my modest point throughout this entire debate is this: Whatever “economic shock” we are talking about in such a scenario, it is not simply, “Foreigners want to reduce their exposure to the USD itself.” To repeat, it would be one thing if people in South America wanted to sell their holdings of Eurodollars and instead hold actual Treasuries. I agree that that change in preferences, would imply a strengthening USD.

But that’s not what Jim Rickards and I were talking about in our ZeroHedge debate. No, we were talking about a scenario where people in South America (and elsewhere) want to reduce their exposure to Eurodollars and their exposure to actual Treasuries. For that type of a preference change, there’s no reason to suppose that their debtors (i.e. those who owe them USD) will suddenly find it more difficult to repay their obligations. On the contrary, the general drop in global demand to hold USD will make the global “price” of the USD fall, making it easier for debtors to satisfy their dollar-denominated obligations.

To sum up: The existence of (fractional reserve) USD obligations makes the analysis more complicated, but nonetheless, a global drop in demand for USD exposure will lead, other things equal, to a fall in the dollar against other currencies. Analysts like Brent Johnson who keep arguing that deleveraging will lead to dollar destruction are conflating two different scenarios. Global events may indeed unfold according to the pattern Johnson describes, but in such a case investors must have shifted in their preference for more direct USD claims versus more tenuous ones. But a general desire among foreign institutions to rid themselves of dollars per se will clearly lead to a fall in the dollar.

Dr. Robert P. Murphy is the Chief Economist at infineo, bridging together Whole Life insurance policies and digital blockchain-based issuance.

Twitter: @infineogroup, @BobMurphyEcon

Linkedin: infineo group, Robert Murphy

Youtube: infineo group

To learn more about infineo, please visit the infineo website

Comments