Whole Life Insurance for the Business Owner

In this outlet, I often explain that at infineo we help businesses set up customized Whole Life insurance policies. I’ve devoted posts to several different aspects of the approach, but I realized I haven’t ever written a stand-alone article summarizing the advantages to a business owner. That’s what I’ll do in the present post.

Explaining the Mechanics of a 10-Pay Whole Life Policy

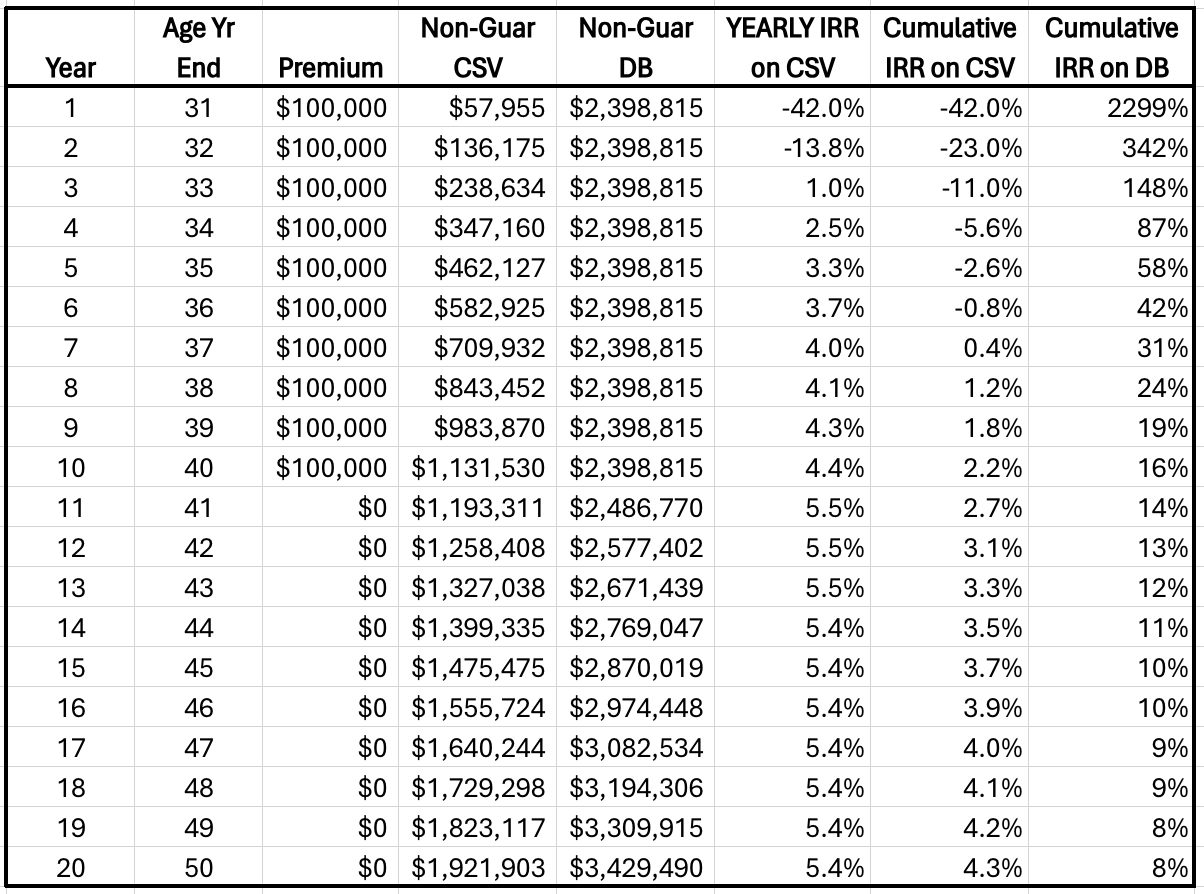

Consider the following illustration that we recently created using the home office software from a major US mutual life company. Note that this particular policy design wasn’t chosen with a specific business in mind—we were using it for a different analysis—but it still provides a useful reference point for our current discussion:

The above shows the first 20 years of projected performance of a 10-pay Whole Life policy (meaning that it contractually only requires ten years of premium payments). Furthermore, this specific design involved a 64/36 base/PUA split, meaning that the actual premium payment necessary to keep the policy in force each year is only $64,000, while the other $36,000 shown is the exercise of a Paid-Up Additions rider. These one-shot bursts of additional (and optional) premiums buy fully paid-up insurance, which boosts the death benefit without further need of premium payments1.

The CSV column stands for “Cash Surrender Value,” and shows what the policyholder could get if he decided to turn in the policy back to the carrier. (This is also the ceiling that determines how much the policyholder can borrow from the carrier, with the CSV serving as the collateral on the loan.) As is well-known, the early years of a Whole Life policy do not exhibit an attractive rate of return on the cash value. Intuitively, this is when the carrier pays for much of the overhead, including the commission to the agent who sold the policy. (To be clear, with these illustrations “what you see is what you get”: there aren’t management fees levied on top of these numbers; such items are already taken into account.)

However, the table shows that looking at the yearly internal return, it accelerates and hits 4.0% by Year 7, and 5.5% by Year 11. Even taking into account the dismal early years, the cumulative IRR (shown in the next column) breaks 4.0% by Year 17.

1 Note that there is some complexity under the hood with this particular policy. Because it’s a 10-pay already, adding in the feature of a base/PUA split required us to put in a declining term rider, in order to maintain the tax advantages of the policy. That is why the death benefit is constant for the first 10 years: What’s really happening is that the amount of one-year term insurance keeps declining as the paid-up additional insurance keeps accumulating, and the term component is fully phased out after the tenth year. I’m discussing this complexity not to intimidate the newcomer, but rather to show that even these “simple” Whole Life policies can have a lot of moving parts, which is why you only want to talk with insurance professionals who are experts at designing them.

Just the Cash, Ma’am

Even if we temporarily put aside the death benefit and view the above policy purely as a fixed-income vehicle, these numbers could be appealing to certain business owners, for several reasons. First, so long as the policy is handled correctly, under current IRS treatment the internal growth is not a taxable gain. If and when the owner wants to access the accumulating wealth, he can begin drawing out dividends up to the cost basis (in this example, the million dollars eventually paid in as premiums), at which point the owner can begin borrowing against the policy. Since loans aren’t income, they don’t trigger tax liability either. This method of building up an asset that grows with advantageous tax treatment and then borrowing against it to fund expenses is precisely how the big boys like Warren Buffett enjoy a jetsetter lifestyle while keeping their effective tax rate low.

However, even though there are plenty of investment strategies that borrow against assets, this technique is particularly simple when the underlying asset is Whole Life insurance. When a policyholder requests a policy loan, the carrier is contractually obligated to oblige. Further, the carrier doesn’t run any credit checks, doesn’t verify income, doesn’t ask what the loan is for, and doesn’t even require a formal payback schedule. In contrast, if a “house flipper” wants the banks to lend against the equity in her rental properties, she may have to jump through such hoops before getting the money.

The reason for this stark contrast in treatment is the nature of the underlying collateral. With a life insurance policy loan, the carrier itself is guaranteeing the collateral. It is literally impossible for the borrower to default because at some point the policy will either be surrendered or the insured will die. Either way, the carrier pays itself back the policy loan (plus any accumulated interest) before giving the net Cash Surrender Value or death benefit to the relevant recipients. Payback involves a simple subtraction problem.

When it comes to conventional bank lending against real estate, the collateral could collapse in price. In any event, if the borrower stops making the payments on the loan, ultimately the bank will have to evict the residents and sell the property. This is a disagreeable, time-consuming process that the bank wishes to avoid, and hence its loan officers exercise discretion on the front end when granting credit.

This discussion leads to the next point: Business owners who currently rely on bank lines of credit would do well to start funding a Whole Life policy. In the example above, even during the first year, there would be $57,955 (less a margin for safety) that the owner could borrow at an attractive interest rate. Rather than funding more traditional savings vehicles, the business owner could redirect $100,000 per year into bulking up a Whole Life policy that would allow the owner to gradually wean himself from reliance on outside banks. This strategy would prove especially wise in the midst of a financial crisis when credit freezes up.

Another huge advantage to the business owner from a Whole Life policy is that its future cash value is relatively safe and predictable. I haven’t shown it in the table above, but there is a contractually guaranteed minimum growth built into the policy. Beyond that, there are projected dividend payments that can be used to allow the policy (meaning both the cash value and the death benefit) to grow more quickly. Even though the dividend payment is not guaranteed, most mutual companies have long histories—dating back decades—of making dividend payments.

Furthermore, whenever a dividend is paid, and thus boosts the cash value of the policy, this sets a new floor on the policy’s value. Wild swings in the stock market don’t affect it, and even interest rates have no effect on the market value of a Whole Life policy. This makes Whole Life safer than even a fund of Treasury securities, with respect to interest rate risk. (Just ask Silicon Valley Bank if Treasuries are really the “risk-free” asset.)

Finally, a robust Whole Life insurance policy is an excellent cash management vehicle for a business owner because it will be around as long as the owner (assuming the owner is the same person as the insured). Individual bonds eventually mature and return the principal, and possibly coupon payments along the way. Bonds are hence a “leaky bucket” for receiving inflows of cash, whereas a Whole Life policy is the preeminent “Warehouse of Wealth” in Nelson Nash’s felicitous phrase.

But Remember, It’s Life Insurance

In the above section, I focused on some of the key “living” benefits a business owner could enjoy from the cash value element of a Whole Life policy. But of course, we are fundamentally talking about life insurance, meaning that the death benefit is the essential feature. As the final column in the table above demonstrates, the rate of return on the death benefit is remarkable if the insured happens to die early.

In a business setting, it can be very helpful to have a large death benefit for the owner, which in the above example is $2.4 million right out of the chute, and which grows to $3.4 million by Year 20. If there are other partners in the business, they could be named as beneficiaries, to receive the proceeds income-tax-free in the event that the insured partner dies.

Even if the business owner is a solo entrepreneur, he may want to use the policy—perhaps in conjunction with a trust—to pass wealth on to the next generations in his family, just as the Rockefellers famously did.

The beauty of life insurance as an asset is that it comes riding in precisely during the scenario when other assets have not had time to gestate. As Austrian School economist Huerto de Soto puts it:

The social significance of life insurance companies sets them apart from other true financial intermediaries. In fact the contracts offered by these institutions make it possible for broad layers of society to undertake a genuine, disciplined effort to save for the long term. Indeed life insurance provides the perfect way to save, since it is the only method which guarantees, precisely at those moments when households experience the greatest need (in other words, in the case of death, disability, or retirement), the immediate availability of a large sum of money which, by other saving methods, could only be accumulated following a very prolonged period of time. With the payment of the first premium, the policyholder’s beneficiaries acquire the right to receive, in the event of this person’s death, for instance, a substantial amount of money which would have taken the policyholder many years to save via other methods. (de Soto, Money, Bank Credit, and Economic Cycles, p. 586)

In sum, there are many advantages for business owners to incorporate a customized Whole Life policy into their financial plan. To receive a no-commitment recommendation tailored to your specific business situation, book a call with one of our experts at infineo.

NOTE: This article was released 24 hours earlier on the IBC Infinite Banking Users Group on Facebook.

Dr. Robert P. Murphy is the Chief Economist at infineo, bridging together Whole Life insurance policies and digital blockchain-based issuance.

Twitter: @infineogroup, @BobMurphyEcon

Linkedin: infineo group, Robert Murphy

Youtube: infineo group

To learn more about infineo, please visit the infineo website

.png?width=520&height=294&name=New%20Article%20Thumbnails%20(17).png)

.png?width=520&height=294&name=New%20Article%20Thumbnails%20(26).png)

Comments